โลกยุคหลัง Covid-19 เริ่มกล่าวถึงเรื่อง”ความยั่งยืนทางการคลัง” (Fiscal Sustainability) มากขึ้นเรื่อย ๆ คำ ๆ นี้นับเป็นหัวใจสำคัญของมาตรฐานการตรวจเงินแผ่นดินที่ INTOSAI พยายามเน้นย้ำเสมอ

ผู้เขียนได้ศึกษารายงานการตรวจสอบขององค์กรตรวจเงินแผ่นดินหรือ SAI ในหลายประเทศที่เผชิญความท้าทายต่าง ๆ เช่น พลวัตประชากร ความเปราะบางผันผวนในการบริหารการคลังยุคใหม่ รายงานการตรวจสอบเหล่านี้พบข้อตรวจพบคล้าย ๆ กันจนสามารถสรุปเป็น “กับดักสามชั้น” หรือ The Triple Trap ซึ่งเป็นสัญญาณเตือนภัยที่แสดงออกมา ดังนี้

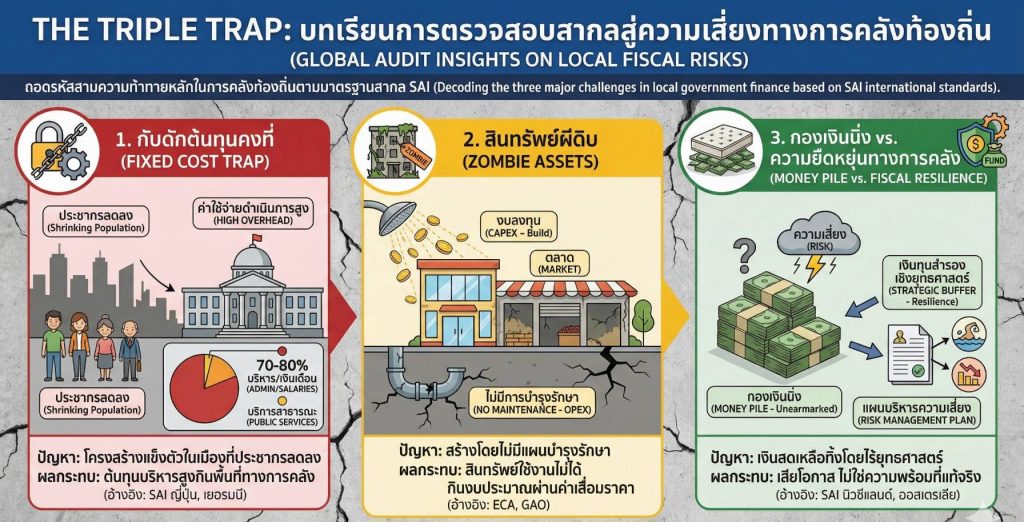

1. The Fixed Cost Trap: เมื่อโครงสร้างรัฐ “แข็งตัว” ท่ามกลางเมืองที่หดตัว

รายงานการตรวจสอบของ SAI Japan (Board of Audit) และ SAI Germany (Bundesrechnungshof) ชี้ให้เห็นถึงอันตรายของการไม่ปรับขนาดองค์กรตามจำนวนประชากรที่ลดลง ผู้ตรวจสอบมองว่าในเมืองที่ประชากรลดลง (Shrinking Cities) ต้นทุนคงที่ในการบริหารจัดการ (Administrative Overhead) กลับพุ่งสูงขึ้นอย่างรวดเร็ว เนื่องจากกฎหมายและระเบียบที่บังคับให้ต้องมีโครงสร้างขั้นพื้นฐานเต็มรูปแบบ พวกเขาชี้ให้เห็นว่า ท้องถิ่นติดอยู่ในกับดักที่ต้องจ่ายเงินเดือนและค่าดำเนินงานสำนักงานเป็นสัดส่วนสูงถึง 70-80% ของงบประมาณ ทำให้ “พื้นที่ทางการคลัง” (Fiscal Space) สำหรับการบริการสาธารณะใหม่ ๆ หายไปอย่างสิ้นเชิง

2. Zombie Assets: กับดักสินทรัพย์ที่ “กินตัวเอง”

SAI ในกลุ่มสหภาพยุโรป (ECA) และ GAO ของสหรัฐอเมริกา มักพบประเด็นการลงทุนที่เน้นการสร้างใหม่ แต่ขาดแผนการบริหารวงจรชีวิตสินทรัพย์ (Asset Lifecycle Management) ผู้ตรวจสอบมักพบว่าท้องถิ่นได้รับงบประมาณมาเพื่อ “สร้าง” (Capital Expenditure) แต่ไม่มีงบประมาณเพียงพอเพื่อ “ซ่อมบำรุง” (Maintenance) ส่งผลให้สิ่งก่อสร้างเหล่านั้นกลายเป็น Zombie Assets คือสินทรัพย์ที่ยังมีชื่อในบัญชี แต่ในความเป็นจริงเสื่อมสภาพจนใช้งานไม่ได้ หรือมีค่าบำรุงรักษาสูงกว่าประโยชน์ที่ได้รับ ผลที่ตามมา คือ กับดักของการสะสมสินทรัพย์ที่ไม่ได้ใช้งาน (Idle Assets) สร้างภาระค่าเสื่อมราคาและค่าดูแลรักษาที่ไร้ประสิทธิภาพในงบการเงิน กลายเป็นภาระทางบัญชีที่กดทับสถานะการคลัง

3. Money Pile vs. Fiscal Resilience หรือ กับดักการสะสมเงินสดที่ไร้ยุทธศาสตร์

SAI New Zealand และ SAI Australia ให้ความสำคัญอย่างยิ่งกับเรื่อง “Strategic Cash Management” โดยแยกแยะระหว่าง “ความมั่งคั่ง” กับ “ความพร้อม” รายงานการตรวจสอบของทั้งสองประเทศ พบว่า ท้องถิ่นหลายแห่งมีเงินสะสมจำนวนมหาศาล (Cash Surplus) แต่กลับไม่มีแผนรองรับความเสี่ยง (Risk Management Plan) ที่ชัดเจน เมื่อเกิดวิกฤตการณ์ทางเศรษฐกิจหรือภัยธรรมชาติ กลับไม่สามารถใช้เงินนั้นได้อย่างมีประสิทธิภาพ

กับดักที่ว่านี้ คือ การเก็บเงินไว้เฉยๆ (Money Pile) โดยไม่มีวัตถุประสงค์ (Unearmarked) ไม่ใช่ความเข้มแข็ง แต่คือ “การเสียโอกาสทางการคลัง” ในขณะที่ Fiscal Resilience ที่แท้จริง คือ การมีเงินทุนสำรองที่ผูกโยงกับแผนเผชิญเหตุและการลงทุนในโครงสร้างพื้นฐานที่ยืดหยุ่น

รากฐานความคิดเรื่อง The Triple Trap จากกรณีศึกษาต่างประเทศสะท้อนให้เห็นว่า ปัญหาทางการคลังไม่ได้เกิดจากการขาดแคลนงบประมาณเสมอไป แต่บ่อยครั้งเกิดจาก “โครงสร้างที่ขาดความยืดหยุ่น” และ “การมองข้ามวงจรชีวิตของเงินและสินทรัพย์” การที่ SAI นำแนวคิดเหล่านี้มาใช้ในการวิเคราะห์รายงานการเงินย่อมช่วยยกระดับบทบาทจากการเป็นผู้ตรวจสอบแบบเดิมไปสู่การเป็น “ที่ปรึกษาเชิงยุทธศาสตร์” (Strategic partnership) ที่ช่วยเตือนให้ท้องถิ่นหลุดพ้นจากกับดักเหล่านี้ได้ทันท่วงที

บทความโดย Dr. Sutthi Suntharanurak 11 ม.ค.69

https://thailandtoday2020news.blogspot.com/2026/01/triple-trap.html

The Triple Trap recognizes local fiscal “traps” through foreign audit reports, by Dr. Suthi Sunthornarak

The post-Covid-19 world has begun to mention more and more “fiscal sustainability.” This word is at the heart of INTOSAI’s always trying to emphasize.

The authors studied the audit reports of the Financial Supervisory Service (SAI) in many countries facing challenges such as population dynamics, fragility in modern fiscal management. These audit reports have found similar findings that can be summarized as “three-tiered traps” or The Triple Trap, alarms expressed as follows:

1. The Fixed Cost Trap: When the State Structure “Solidifies” Among Shrinking Cities

The audit reports of SAI Japan (Board of Audit) and SAI Germany (Bundesrechnungshof) indicate the danger of not scaling organizations with declining populations. Auditors view that in Shrinking Cities, administrative overhead has skyrocketed. Due to laws and regulations that enforce full infrastructure, they point out that localities are caught in traps requiring 70 to 80 percent of the budget’s salary and office operating costs, completely disappearing the “Fiscal Space” for new public services.

2. Zombie Assets: The “self-eating” asset trap.

SAI in the European Union (ECA) and GAO of the United States often find investment issues focused on rebuilding, but lack of Asset Lifecycle Management plans. Inspectors often find that local governments are budgeted for “Capital Expenditure” but do not have enough budget to “maintenance” to turn those buildings into Zombie Assets. It is an asset that still has a name in the account, but in reality deteriorates to an unusable level or has a higher maintenance cost than the resulting benefit. The trap of accumulating idle assets creates an inefficient depreciation and maintenance burden on the financial statements.

3. Money Pile vs. Fiscal Resilience or strategic cash collection trap

SAI New Zealand and SAI Australia put great importance on “Strategic Cash Management” by distinguishing between “wealth” and “availability.” The two countries’ audit report found that many regions have a large cash surplus, but do not have a clear risk management plan in the event of an economic crisis or natural disaster. Can’t afford to spend that money efficiently.

This trap is to keep money Pile without purpose (Unearmarked) not strength but “fiscal opportunity loss” while real Fiscal Resilience is to have reserves linked to contingency plans and investment in flexible infrastructure.

The Triple Trap foundation from international case studies shows that fiscal problems are not always caused by budget shortfalls, but often by “inflexible structures” and “overlooking the life cycle of money and assets.” The SAI’s use of these concepts in financial reporting analysis enhances its role as a traditional auditor. “Strategic partnership” that reminds the locals of their immediate release from these traps.

บทความโดย Dr. Sutthi Suntharanurak 11 ม. C.69…